Every month we take a closer look and drill down the sales data of Ottawa condos from the previous month. Here are the statistics for March 2026 in the top five "downtown" areas - Centretown, Byward Market and Sandy Hill, Little Italy (which includes Lebreton Flats), Hintonburg, and Westboro. The information will be specific to apartment-style condominiums, and only what is sold through the MLS. Also important to note that DOM (Day's On Market) is calculated to include the conditional period, which in Ottawa is roughly 14 days for almost every single transaction.

Ottawa’s housing market showed clear signs of early spring momentum in March, with sales activity picking up after a slower winter and pricing beginning to firm across several segments.

While overall conditions remain balanced, the data suggests that demand is starting to re-engage as we move into the spring market. Buyers still have options, but the window of slower, less competitive conditions may be narrowing.

Sales Activity Begins to Rebound

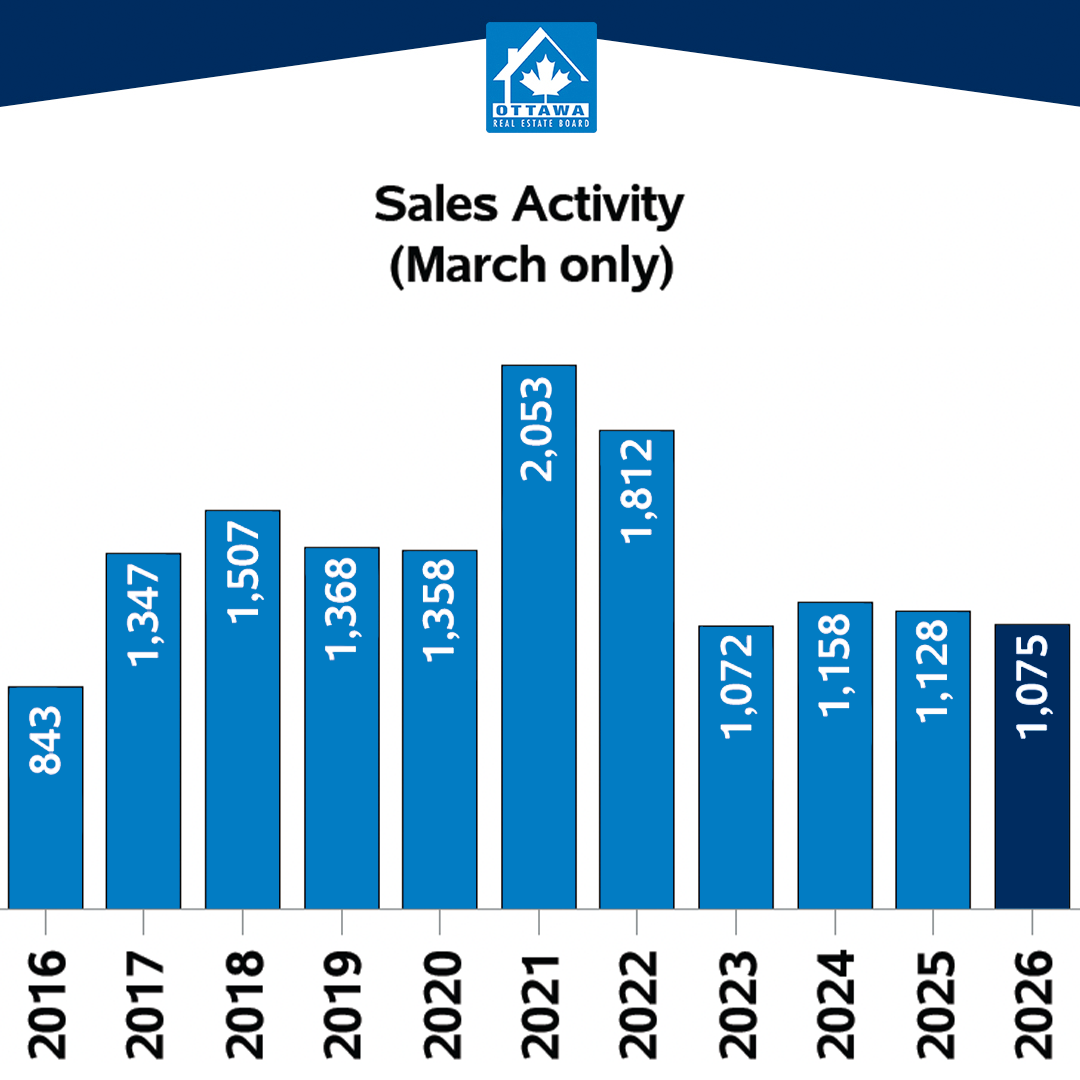

A total of 1,075 residential properties sold in March 2026, representing a 4.7% decrease compared to March 2025, but a meaningful improvement from February’s slower pace.

Although sales are still slightly below recent March levels, they are now back within range of prior years:

2025: 1,128 sales

2024: 1,158 sales

2023: 1,072 sales

This indicates that while the market has not fully returned to peak activity, it is stabilizing and moving in a more typical seasonal direction.

Notably, single-family homes led the recovery, with 562 sales in March, matching last year’s performance and significantly improving from February.

Inventory Remains Elevated, But Is Being Absorbed

Supply continues to build across the Ottawa market, but stronger sales are helping to keep pace.

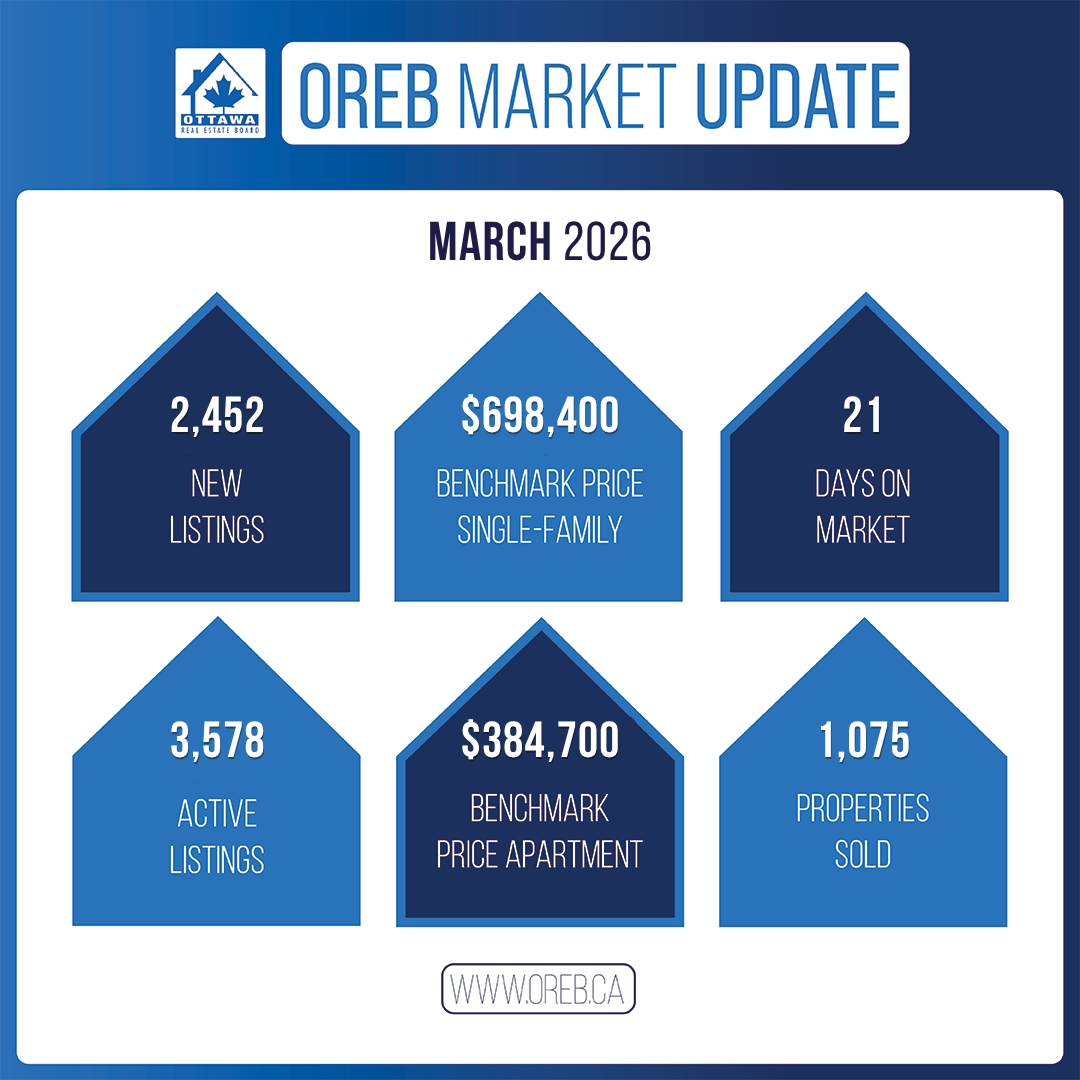

2,452 new listings came to market in March, up 7.5% year over year

3,578 active listings were available at month-end, up 10.3% year over year

Despite this increase in inventory, conditions are not loosening further. Instead, the market is starting to tighten slightly due to improved absorption.

Months of inventory dropped to 3.3, down from 3.8 in February, which keeps Ottawa firmly in balanced territory.

This is an important shift. While buyers still have more choice than in recent years, that choice is beginning to shrink as demand picks up.

Prices Show Early Signs of Strengthening

Headline pricing in March remained relatively stable, but underlying trends point to strengthening values.

Average sale price: $692,584 (up 0.9% year over year)

Median sale price: $642,000 (down 0.5% year over year)

On the surface, these numbers suggest modest movement. However, the MLS® Home Price Index (HPI) provides a clearer picture.

Benchmark prices increased month over month across:

Composite market

Single-family homes

Apartment/condo segment

Townhomes remained stable.

Because the HPI adjusts for the mix of properties sold, these increases suggest that true market values are beginning to firm, not just seasonal price fluctuations.

Market Conditions by Property Type

Different property types continue to behave differently, which is shaping how buyers and sellers experience the market.

Single-Family Homes

Detached homes remain the most stable segment. Inventory tightened to 3.0 months, and pricing has held steady. Demand is strongest in this category, particularly at accessible price points.

Townhomes

Townhomes continue to see steady demand, with 2.8 months of inventory, indicating relatively competitive conditions. This segment remains attractive to buyers looking for a balance between affordability and space.

Apartments and Condos

The condo market is still carrying higher supply, with 5.5 months of inventory, but there are early signs of improvement. Rising benchmark prices and better absorption suggest that this segment may be starting to stabilize after a slower period.

What This Means for Buyers

Buyers are still in a relatively favourable position compared to the past few years.

There is more inventory available, and less urgency than during peak market conditions. However, the data suggests that this window may be narrowing.

As sales activity increases and inventory is absorbed more quickly, competition is likely to build gradually through the spring.

What This Means for Sellers

Sellers are entering a more favourable market than earlier in the year.

Demand is strengthening, particularly for freehold properties, and well-priced homes are seeing consistent activity.

The key difference compared to past peak markets is that pricing strategy matters more. Buyers are still selective, and homes that are overpriced may take longer to sell.

Looking Ahead to Spring 2026

March data confirms that Ottawa’s housing market is transitioning out of its slower winter phase.

Sales are improving

Inventory is being absorbed more effectively

Benchmark prices are beginning to rise

Conditions remain balanced

National forecasts, including CREA’s 2026 outlook, point to gradually strengthening demand as borrowing conditions ease. Ottawa’s recent performance aligns with that trajectory.

If current trends continue, the spring market is likely to bring steady momentum rather than a sudden surge, with balanced conditions supporting both buyers and sellers.

Important to note is that these statistics can only be as accurate as there are condos sold in Ottawa. The more condos sold in an area, the more accurate the averages will be.

Want to chat about your options? Fill out the form at the bottom of the page, or text/call us directly at 613-900-5700 or fill out the form at the bottom of the page.

Do you have any questions about how this information affects your investment or looking for more information to make the best decision about your purchase? Let’s chat! Fill out the form on the bottom of the page.